The retailer’s involvement in accounting occurs only at the point of sale, which reflects on the balance sheet. At that juncture, the revenue from the sale and the payment to the supplier are recorded. In a sale or return arrangement, the consignee takes possession of the goods with the option to return any unsold items to the consignor. This type of consignment is particularly beneficial for retailers who want to test new products without committing to a full purchase. The consignor retains ownership of the goods until they are sold, which means the consignee does not record the inventory on their balance sheet.

Reversal of writedowns allowed under IAS 2; prohibited under US GAAP

This is because there is no change in ownership, as far as the initial transfer is concerned. However, it is preferable to record a change in location of the inventory, in order to ensure that it is properly recorded. As far as the consigner is concerned, it is defined as the party that takes ownership of the stock.

The Benefits of Consignment Inventory For Consignors in 2023

Also, free up storage space for extra inventory before it arrives if you’re introducing a new product. The consignee assumes many risks because a retailer is ready to take on most of a product’s stock. In order to make the most of consignment inventory, retailers should take the following steps to ensure a mutually beneficial arrangement. Typically, when selling inventory on consignment, the consignor will look for a store or website that caters to their target customer and already has a large customer base. These factors offer a better chance that the product will sell and the consignor will get paid. It also means that the consignor can get their product in front of more potential customers by capitalizing on the consignee’s already established brand.

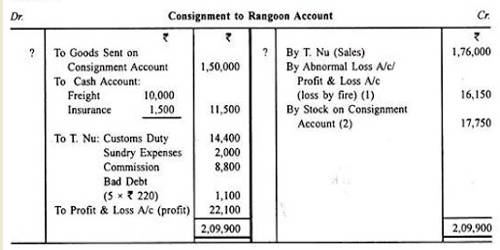

Consignment Accounting – Initial Transfer of Goods

Plus, you can easily integrate it with all your existing business software for a fully connected system that updates itself in real-time. When it comes to the accounting treatment of consignment inventory, the standards are clear about it. Since the risks and rewards of the goods do not transfer due to the transfer, the consignor cannot record the inventory as sold. Inventory represents a significant part of the balance sheet for many companies. In accounting for inventory determining and capturing the costs to be recognized as an asset through the inventory lifecycle is key, because it affects a company’s KPIs such as gross profit margin. Despite similar objectives, IAS 21 differs from ASC 330 in a number of areas2.

It can help you track all of every part of the consignment accounting process. Consignment inventory includes goods that one company owns but are kept or kept by another company. The company that owns the goods is the consignor, while the company that holds them is the consignee.

- Plus, you can easily integrate it with all your existing business software for a fully connected system that updates itself in real-time.

- The selling and commission expenses relate only to goods which have been sold and can be taken direct to the appropriate expense account.

- When a sale occurs, the consignee records the revenue and the cost of goods sold, while the consignor recognizes the sale and removes the corresponding inventory from their balance sheet.

- The accounting for the costs of transporting and distributing goods to customers depends on whether these activities represent a separate performance obligation from the sale of the goods.

By diversifying your inventory with consigned goods, you can reduce risk while providing your customers with new and exciting products. Consignment inventory is different from a wholesale distributor because the consignor — the owner of the product — only gets paid if the product sells. In wholesale transactions, the owner of the product (or inventory) is paid upfront by the retailer that wants to sell its goods. They buy a specific set of units from the wholesaler for a set price per unit, knowing they will add a markup when selling it retail.

The contract covers the item cost, shipping fees, return procedures, inventory management, deposit or commission requirements, and liability for lost or damaged products. Since 2016, Qoblex has been the trusted online platform for small and medium-sized enterprises (SMEs), offering tailored solutions to simplify the operational challenges of growing businesses. With a diverse global team, Qoblex serves a customer base in over 40 countries, making it a reliable partner for businesses worldwide.

Therefore, it is not included in the consignee’s inventory balance until a sale occurs. Xledger provides a cloud-based financial software solution perfectly poised to manage consigned inventory. Consigned goods enable businesses to maintain an adaptable inventory that can quickly respond to changes in tax tips for resident and non 2020 demand and market conditions. Upon receipt of the consigned goods, the consignee records them as inventory with an offsetting liability to the consignor on their balance sheet. The value of the inventory is determined by either the consigned price or the estimated market value, whichever is lower.

Maybe you’re established, but the retailer doesn’t know you and is hesitant to hand over a fat check to purchase some of your products wholesale. A shoe store might collaborate with a small designer to sell some of the designer’s products in-store. In this scenario, the retailer doesn’t need to order the shoes themselves, and the designer manages the consignment stock.